Tax Advisory

Tax Advisory vs Tax Audit

Tax intelligence provider, Tolley, offers answers and guidance for tax specialists, throughout their tax career. It also helps tax professionals understand and predict changes in the market. One such change is the shift towards business advisory. Amir Belal and Matthew Leopold from LexisNexis comment

Business advisory is nothing new in the tax accountancy world - many accountants already offer business advisory services. In a Sage 2020 report, 79% of accountants said they are confident or very confident in providing business management advice, while 63% are training or planning to train around financial business advisory services.

Source: Sage

Melissa Johnson

Principal, Assurance and Financial Reporting, Rehmann

Charles Story

Director, Operations for Corporate Investigative Services, Rehmann

Advisory matters now account for around two-thirds of work, where previously compliance made up the bulk of work, says Karen Campbell-Williams, head of tax at Grant Thornton.

"Although we talk about the simplification of the system, there is more and more of it, and it's more and more complex," says Campbell-Williams. "Just the quantity of the tax law has grown enormously. In order to be able to file a corporate tax return, there's quite a lot of add-on advisory that clients need, if they're going to get that right."

Client activities are also changing; clients are buying and selling more and employing more people. The world is becoming more global, and clients are sending more people to other countries, etc.

Clients need to interpret complex tax laws correctly; are we doing it right? And are we accessing the tax reliefs available to us and maximising the available benefits?

"A lot of businesses historically were missing out on those types of claims and reliefs because they weren't getting the specialist advice as to what you can claim and what you should claim," says Campbell-Williams.

At the same time, companies are also becoming more concerned about the optics of their tax arrangements if they are seen to be aggressively minimising their tax burden, particularly in the current economic climate.

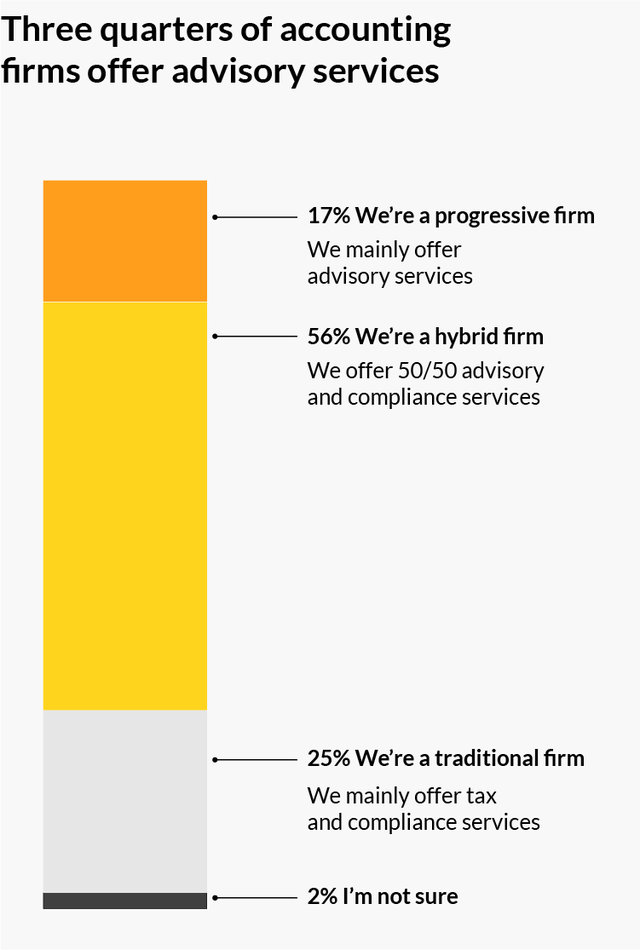

Clients often consider accountants the most trusted advisors to navigate the complex system, and three-quarters of accounting firms offer advisory services.

Does your accountancy firm have what it takes to offer advisory services?

While general tax practices may need scale to support an advisory business, London-based Finerva is proof that smaller advisory firms can thrive by offering specialist or niche services that clients can't find elsewhere.

"It doesn't come down to how big you are—we are referred work from one of the big four [accountancy firms], and we regularly win clients from top 10 firms," says Adam Brodie, Finerva's co-founder and CEO.

"Professional services is about personal relationships; that is still king. The role of the accountant is the most trusted advisor, so if clients are just looking for someone who is going to help with their compliance, then there is a risk that's going to be a short-lived relationship anyway."

A potential challenge that some accountancy firms may face is that they have always offered advisory services as part of their broader compliance work but have never charged separately for those services. They don't have formal fee structures in place to help their clients with business advisory services, meaning they are missing out on revenue opportunities.

"What people have generally struggled with is the definition around advisory," says Glenn Collins, head of policy, technical and strategic engagement at the Association of Chartered Certified Accountants. "Many accountants undertake advisory work, but they don't recognise it."

"It's knowing when to stop that conversation before moving on to the next area," says Collins.

For tax professionals and clients, that means clarifying where compliance stops and advisory starts—and understanding how to charge for it.

"We've done it".

One example of an accountancy firm that took the plunge into advisory services is HURST, a 100-people, medium-sized firm based in the northwest of England, principally in Manchester and Stockport.

"We originally started as a fairly traditional accountancy audit firm, but our specialist advisory teams have really grown in the last six or seven years to be a significant part of the business", says Adrian Young, a tax partner at Manchester and Stockport-based accountancy firm at HURST.

"What we're finding is that as we help our clients get bigger and bigger and more sophisticated, they inevitably need more advisory services as well as the standard compliance work."

"The impetus really came from two sides," says Young. The greater need for advisory services as our clients become larger and more sophisticated. And then internally, as people develop, they want more interesting work.

There's also a financial imperative to that. Compliance is more about price, whereas advisory work is much more about value—what value does this piece of advice bring, rather than what does it cost?

Price vs value

While many firms have already moved to fixed fees for compliance work, advisory services can be more challenging to price up, given that each job is unique. Even so, clients will likely demand to know costs upfront rather than leave the clock running.

"For advisory work, it has to be quoted on a bespoke basis because no two cases are the same," says Brodie. "We would only charge an hourly rate if we couldn't get a handle on the scope or the amount of work, and perhaps they needed us to start work pretty quickly."

Whatever way firms decide to bill their clients, they need to have the appropriate conversation with the client and be clear at the outset what the breakpoint is for compliance work, says Collins.

Are clients getting what they want?

Young believes clients want a "one-stop shop".

The message we get from clients is that they want us to tell them about other things we can help them with - how we can support them and help them achieve what they are trying to achieve, says Campbell-Williams.

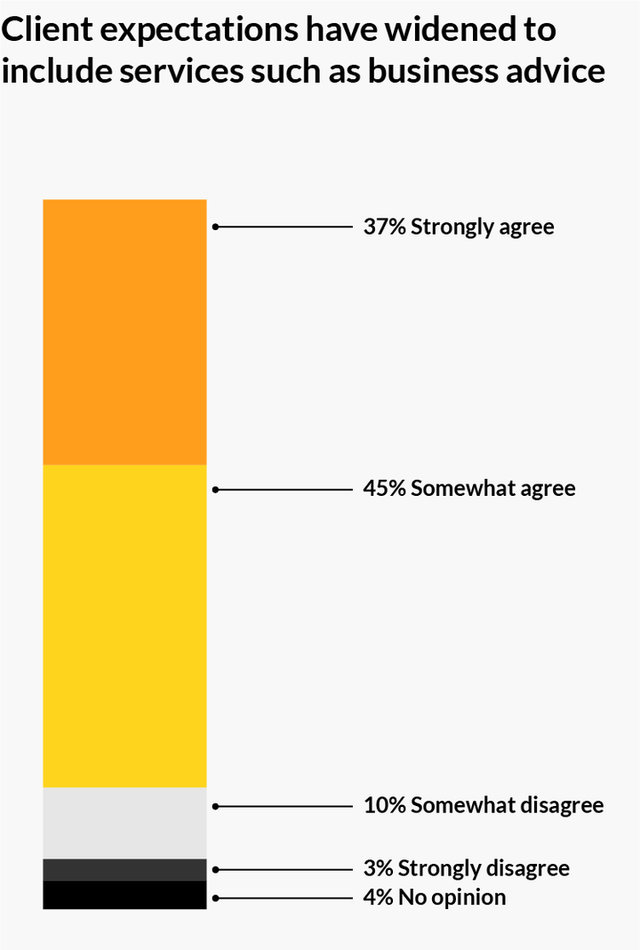

According to Sage 2020, 82% of accountants agree that clients demand a broader service offering to include services such as business advice.

"We use the accountancy firms for a lot more than just audit and tax," says Tamsin Ashmore, CFO at Ultima, an IT services company. "They incorporate all elements of advisory for us, from IFRS conversion projects to due diligence, to cost transformation discussions."

The risks of moving into advisory services

Some clients don't need advisory services.

"Many clients just need an audit, or they just need their tax returns done, so there's always the risk that if you're moving into much more sophisticated areas of work that you do leave some clients behind," says Young. "We mustn't forget that the core of what we as an industry do is the compliance work."

Aggressively cross-selling advisory offerings to existing clients—even if they might benefit—is a potential turn-off if those clients feel they are being pressured into buying additional services.

What do clients want?

If you are considering a move into tax advisory services, you should consider the following tips from expert commentators.

- Understand your clients' needs - your interests must align with their needs. The advice must be relevant to your client.

- Is it worth it for your client? - does it make sense to pay for the advice? "Clients have to be earning enough themselves so that the tax at stake is worth advice for," says Andrew Hubbard, editor in chief of LexisNexis' Taxationmagazine.

- Clients expect expert advice - do you have the expertise and the liability cover to offer professional advice?

The increased complexity of the business and tax world means there is an opportunity for services beyond auditing as clients' need for support and advice from their most trusted advisers - their accountants - will increase.

For accountancy firms that can align their interest with the needs of their clients, the sky is the limit for both the firm and the client.

For the full report on how tax accountants can transition to advisory and other higher-value services and meet clients' demands, read our report at https://www.tolley.co.uk/knowledge-centre/advicepower