Supply Chain risk

The importance of communicating ESG policies

Angela Moliterni, Chartered Accountant and Auditor at BLCI International investigates why companies must adopt circular economy models to meet consumer demands and mitigate future supply chain risks as highlighted by Capgemini Research Institute’s report

T

he report, published at the end of 2021 entitled "Circular economy for a sustainable future: How organisations can empower consumers and transition to a circular economy", confirms the need to change the economic model from linear to circular, showing that more than seven out of ten consumers want to adopt practices such as reducing overall consumption (54%), buying more durable products (72%) and storing and repairing products to increase their lifespan (70%).

The results that emerge indicate an awareness on the part of consumers: worldwide, 45% of those interviewed are ready to support brands that invest in the circular economy, this percentage rises to 50% in Italy and even reaches 74% in India and 62% in China.

It is therefore essential for companies to integrate ESG and circular economy considerations into their business strategies and to communicate their objectives and actions to all internal and external stakeholders.

The importance of ESG communication in Italy

Sustainability reporting today is mandatory for large organisations in Italy (more than 500 employees): the final "Non-Financial Declaration" has to contain data on the environment, human rights, community, personnel and corruption, as provided by Directive 2014/95/EU implemented by the national Legislative Decree no. 254/2016.

For small and medium-sized enterprises, even if there is no formal duty to report, it is becoming a compulsory step, as a consequence of external environment changes and of the demands coming from various stakeholders such as banks, suppliers, customers and public authorities.

According to a survey published by the Forum for Sustainable Finance (FSF) in collaboration with BVA DOXA in 2020, SMEs in Italy have shown increasing attention to ESG issues. 65% of the companies surveyed have already introduced a sustainability report as promoted by the GRI Standards and, according to European Directives, unlisted SMEs will also be forced to report on sustainability from 2026.

ESG aspects for many companies are becoming conditions of existence in the medium to long term. Banks are becoming an important player in this process. They are responsible for financing Italian SME’s in the transition to sustainability (according to EBA directives as of 30 June 2021). The presence of quality and ISO certifications is increasingly a strong point for companies applying for funding and important information for banks in their credit assessment process: business continuity and fulfilment of ESG objectives are essential. European legislation also encourages circular economy and green transition actions with grant funding and tax credits, through the Horizon Europe programme (the EU's largest research and innovation programme with a budget of EUR 95.5 billion, which will run until 2027).

We at BLCI provide our clients with professional support in adapting ESG processes. Sustainability has a financial relevance in terms of reducing risks and contributing to the generation of economic and financial value. The sustainability path that we propose to our clients mainly involves three ESG dimensions and in concrete terms is based on:

ENVIROMENTAL

- Definition of measurable targets for energy, water and raw materials consumption reduction;

- Audit and reporting on emissions relating to: (1) gas boilers, company vehicles, plants and Indirect emissions (2) the purchase and use of energy used by the organisation, (3) the organisation’s activities (EU - GHG Protocol);

- Implementation of policies about waste reduction and recycling.

SOCIAL

- Supporting in defining parenthood policies;

- Adoption of corporate welfare systems;

- Implementation of career development paths to support the less represented gender in management roles;

- Partnership agreements with local non-profit organisations and/or support through donations or corporate volunteering for social, environmental and cultural initiatives;

- Assessment procedure adoption for human rights respect in the value chain (as per UN Guiding Principles on Business and Human Rights).

GOVERNANCE

- Identification of management's sustainability role;

- Mapping of relevant ESG risks, updated at least annually;

- Sustainability Reporting;

- Defining of an ethics code and implementation of anti-corruption procedures;

- Integration of the SDGs into the corporate strategy;

- Definition and inclusion of environmental and social criteria in supplier selection and monitoring procedures;

- Products certification according to quality standards.

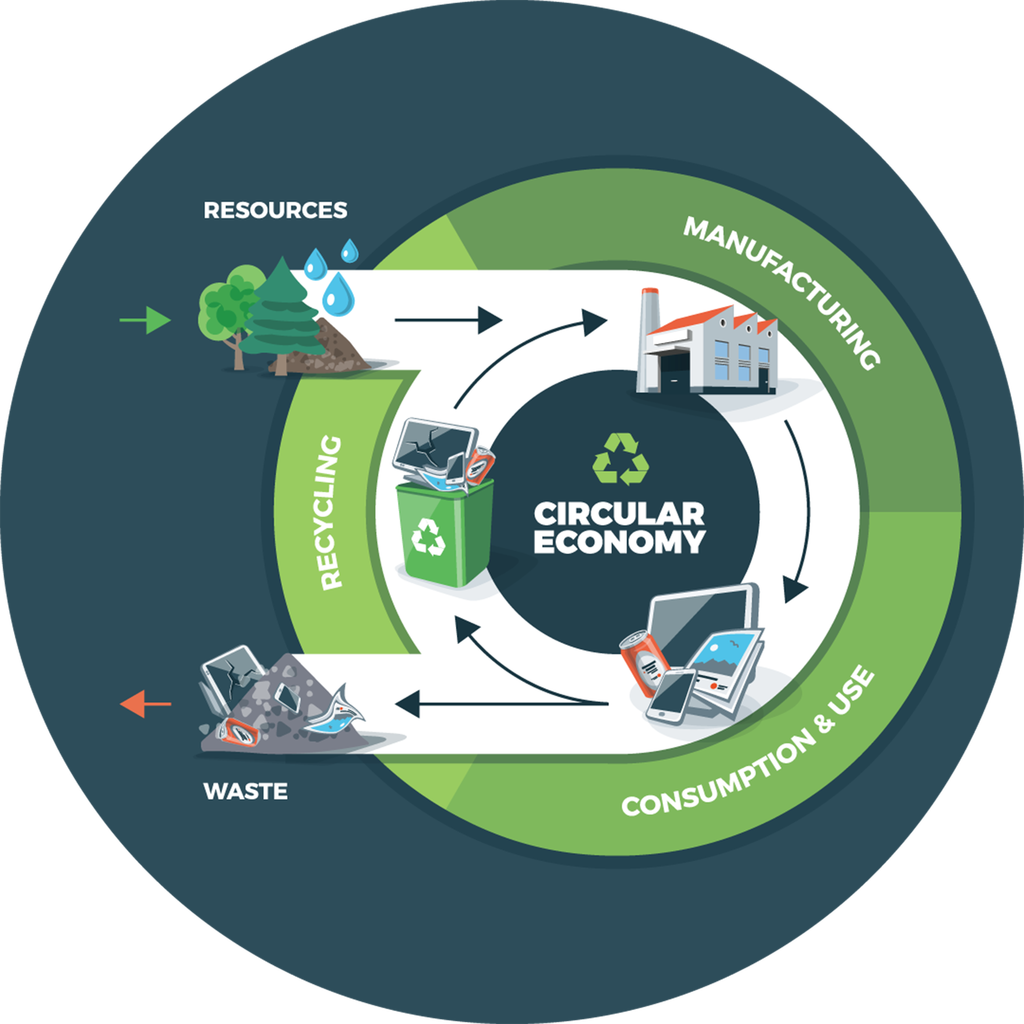

Many of our customers have already adopted an ESG system and are moving forward the circular economy model, recycling raw material waste from which they derive secondary raw materials that they resell for use in a wide variety of sectors, allowing them to gain a greater advantage over their global competitors.

Angela Moliterni

Chartered Accountant and Auditor at BLCI International