Triple Capital Accounting

What is Triple Capital Accounting and why there’s a need for a shift from traditional accounting norms

Laurent Le Pajolec and Christina Tsiarta of Kreston discuss why a firm should engage in TCA and why existing accounting methodologies are no longer sufficient

However, some firms remain cautious of the thought of going down this route. This is understandable due to the rumoured headaches of the claims process, and with HMRC clamping down on risky and potential fraudulent claims. However, whether you’re an accountancy firm or a specialist consultancy, understanding your clients’ eligibility is an easy, seamless process – as long as you break it down into three simple steps.

Understanding triple capital accounting

If there is one language that is truly universal, it must be that of accounting. Accounting norms are the business language used internationally, so that companies can communicate their financial and economic information to stakeholders and make business decisions that affect how they operate, grow and engage in activities. The numbers on a company’s balance sheet mean the same thing across borders, providing a powerful standard means of communication.

However, traditional accounting techniques focus on the financial aspect of a company’s activities, and do not consider the social and environmental impacts of those activities. Similarly, the focus in balance sheets is on financial assets, ignoring the company’s reliance on natural and/or social assets. Plainly put, a company is considered to be successful because it is making a profit in financial terms, regardless of whether it is simultaneously destroying the natural environment and/or negatively impacting social relationships.

The triple capital accounting framework (TCA) proposes that business accounting should apply the concept of preservation of financial capital as displayed in a balance sheet (for example, through depreciation, amortisation or capex), to human and social capital. It does this by adding additional lines to the balance sheet, to count the depreciation of natural and social capital as well. Including natural and social assets in liabilities, guarantees the conservation of such assets, similar to financial capital. Stemming from the world of environmental accounting, TCA is not so much about internalising the environmental and social externalities associated with business activities, but more about appropriately funding the cost of maintaining environmental and social ecosystems. Under TCA, the three types of capital are not interchangeable and non-substitutable; they are all equal independent strategic assets. A company under the TCA framework can therefore value new assets and highlight aspects of its business model that might have been previously undervalued by stakeholders.

Christina Tsiarta, Head of Sustainability, ESG and Climate Change Advisory Services, Kreston Ioannou & Theodoulou

Why should an organisation implement TCA

We are currently amid the greatest ecological emergencies for humanity. In fact, there are nine planetary boundaries that we need to incorporate into our accounting framework in order to ensure the survival of our species and planet; these are climate change, ocean acidification, stratospheric ozone depletion, disruption of the nitrogen and phosphorus cycle, global water use, land use change, erosion of biodiversity, the increase of aerosols in the atmosphere and the introduction of new entities in the biosphere. One of the most prominent boundaries is climate change. At the United Nations Climate Change Conference of the Parties (COP27) in Egypt in November 2022, António Guterres, Secretary-General of the United Nations noted, “Greenhouse gas emissions keep growing. Global temperatures keep rising. And our planet is fast approaching tipping points that will make climate chaos irreversible. We are on a highway to climate hell with our foot on the accelerator.” We are living in a world limited by natural resources. However, we use these resources to produce products and provide services without thinking about how our activities impact the natural environment. This focus has to change.

Similarly, social norms are also shifting. Whether it’s diversity and equal opportunity in the workplace, a stance against harassment (such as the #MeToo movement), practices to eliminate discrimination based on gender, religion, disability, appearance, sexual orientation or sexual identity, human rights due diligence across an organisation’s supply chain, a focus on employees’ (mental) wellbeing and a work-life balance, corporate social responsibility or societal expectations on organisations to be transparent, accountable and responsible in order to have a social license to operate, the business landscape is changing. Organisations are forced to consider how they impact and are impacted by their social capital.

It is not surprising therefore to see evolution in accounting norms. TCA methodologies help an organisation to measure the real impact of its activities and services by incorporating into its decision-making social and environmental externalities, therefore enabling it to work towards becoming more sustainable and resilient. For example, what types of pollution are my activities and products responsible for, either directly or indirectly (e.g. costs to avoid, cost to retreat, etc.)? What is the impact of my activities and products on biodiversity (vegetal and animal species) throughout my supply chain? What resources do I need today and tomorrow to keep producing products and provide services across their life-cycle (e.g. costs from extraction to production, use and disposal at end of life)? What are the social impacts of our products and services (e.g. child labour, human rights violations, community involvement, harassment in the workplace, etc.)? How do we calculate the environmental and social costs of our future investments? What provisions do we need to have in place to ensure the survival of our natural and social capital, alongside our financial capital, in case this becomes mandatory by legislation?

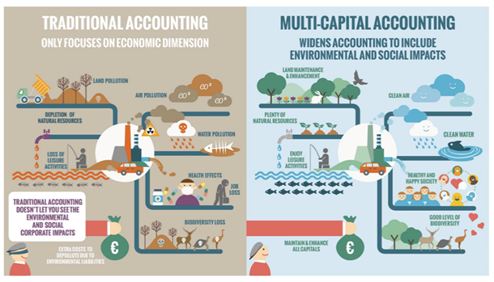

Figure 1 provides a graphical comparison of traditional accounting, which focuses on just the economic dimension, vs the triple (or multi) capital accounting, which also incorporates the environmental and social dimensions.

Figure 1: Traditional accounting versus multi-capital accounting (Fermes d’Avenir, 2019)

The different TCA methodologies currently available

Many different methodologies exist for TCA in practice. We describe in further detail the two most popular ones, the LIFTS model and the CARE model. We also outline a few more TCA methodologies that are currently being used by organisations.

LIFTS model (Limits of Foundations Towards Sustainability):

The LIFTS model comes from the Global and Multi-Capital performance research chair by Audencia (University Nantes, France). This model was designed to help companies to adopt a sustainable socio-environmental system to ensure the sustainability of their activities. To do this, the model allows companies to monitor their integrated performance for two new capitals: social and environmental.

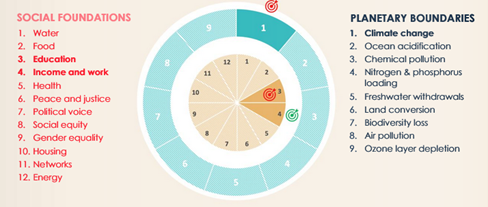

Figure 2: The social foundations and planetary boundaries of the LIFTS model (Audencia - University Nantes, France)

The LIFTS model refers to the Doughnut theory (Raworth, 2017) with the nine planetary boundaries (the ecological ceiling) and the 12 social thresholds (social foundations). The planetary boundaries indicate an environmental budget ceiling that must not be exceeded. The social foundations indicate a social budget floor to be achieved. In this way, the company ensures that its activities do not exceed the limitations of the earth system, nor degrade individuals’ access to their basic needs.

The company’s impacts are split into three categories: “operations”, which comprise the company’s activities; the “supply chain”, which includes the activities of its suppliers; and “products & services”, which include the externalities of the products or services sold by the company. The company is ultimately responsible for its operations, its choices of suppliers and the products and services it provides. The lens of the company’s business model is used to determine areas with a strong potential impact on the boundaries and foundations, upstream of the accounting work. In this way, accounting gives the company an all-encompassing view, allowing it to consider the transformations necessary for becoming more sustainable, while respecting these boundaries and foundations.

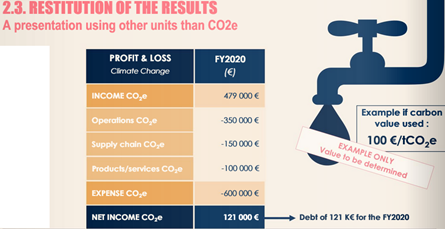

Each company chooses the planetary boundaries and social foundations that better correspond to its sector, and therefore to its monitoring and action priorities. The results are presented per limit/foundation with an associated physical unit (ton of CO2e, €, etc.) within its balance sheet and P&L. The performances calculated on each of the boundaries and foundations do not offset one another. Each result is calculated and analysed separately.

Figure 3: Restitution of the results (Audencia - University Nantes, France)

This model connects financial accounting with environmental and socio-economic issues. Together with the planetary boundaries and social foundations, it tracks multi-capital performance via an accounting system that records activities as physical flows, in parallel with audited financial accounting. The result that is calculated, once contextualised, provides information on the company’s integrated performance.

CARE model (Comprehensive Accounting in Respect of Ecology)

The CARE model (Comprehensive Accounting in Respect of Ecology) was developed by the CARE community, composed of scientists, academics, businesses, and NGOs, gathered around the “Ecological Accountability Chair” and CERCES. The CARE Model is proposing that the balance sheets and P&L of companies, and other performance KPIs, should include the obligation to preserve all CARE "capital assets" - i.e. the natural and human capital employed by companies, alongside the financial capital.

Human and natural capital refers, according to this perspective, to all assets derived from services provided by human beings and by nature, capable of influencing the company’s value creation; these capitals do not refer to human beings or ecosystems in their complexity, integrity and limits.

Human and natural capital are therefore a subset of 'capital' and form a part of what is called immaterial capital, as they are based on 'services' (i.e. immaterial) outside a classical contractual/market framework (human and natural). For example, in the case of human capital (according to this approach), skills are intangible capital because they increase shareholder value and are not governed by an employment contract. A contract discusses the conditions of work, its cost, etc., not the purchase of skills per se (this is negotiated during job interviews). The whole theory of 'skills', at the heart of HR today, is based on this view.

The key indicators considered by the CARE method include the following:

Financial indicators: growth rate, profitability rate, expenditure level, debt level, etc.

Social indicators: unemployment rate, worker participation rate, level of training, quality of customer service, etc.

Environmental indicators: carbon footprint, air quality, water quality, biodiversity, etc.

According to this view, the productivity of assets is theoretically conditioned not only by their direct exploitation, but also by external factors, called externalities. According to CARE, a company can only calculate its profit once the "repayment" of its ecological debt, towards these natural and human capitals, is guaranteed, as it already does for its financial capital. These financial statements are designed to provide companies with a better understanding of their financial, social and environmental capital performance and impacts.

Other methodologies in summary:

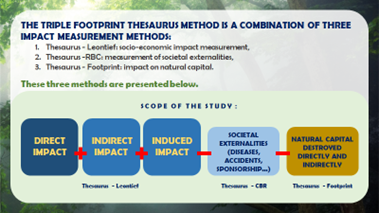

The Triple Footprint Thesaurus method was designed by the firm Goodwill-management group Baker Tilly. The Triple Footprint Thesaurus method is a combination of three impact measurement methods: 1. Thesaurus - Leontief: socio-economic impact measurement ; 2. Thesaurus -RBC: measurement of societal externalities; 3. Thesaurus - Footprint: impact on natural capital. These three methods are presented below.

Figure 4: The Triple Footprint Theasurus Method (Goodwill-management)

Thesaurus-Leontief: this method makes it possible to calculate the socio-economic footprint of a player on its territory with direct but also indirect and induced economic impacts, expressed in euros and in jobs.

Thesaurus - RBC: this method recommends categories of indicators on social externalities to be measured, such as quality of life at work (cost of work-related accidents and illnesses), job insecurity (cost of precarious employment : temporary and fixed-term contracts), sponsorship (gain linked to the sponsorship of skills for the beneficiary company), professional integration (cost of unemployment avoided by the employment of senior and disabled employees), training (gain linked to the training of alternating work experience, cost linked to the absence of training), telecommuting (gain linked to the travel time avoided for employees), gender pay gap (loss of purchasing power for less well paid women), and purchases from the sheltered sector (gain linked to the jobs supported in adapted structures).

Thesaurus - footprint: Goodwill management presents the following categories: greenhouse gas emissions (contribution to global warming), air pollution (PM10, PM25, Nox, NH3, SO2, VOC - reduction of air quality), land use, subsoil and biodiversity (artificial lands, destruction of habitats and raw material extraction), waste management (reduction of landscape quality, water and soil contamination), water pollution (consumption of polluted water or food eutrophication) and water consumption (access to water for local populations, consumption of non-potable water).

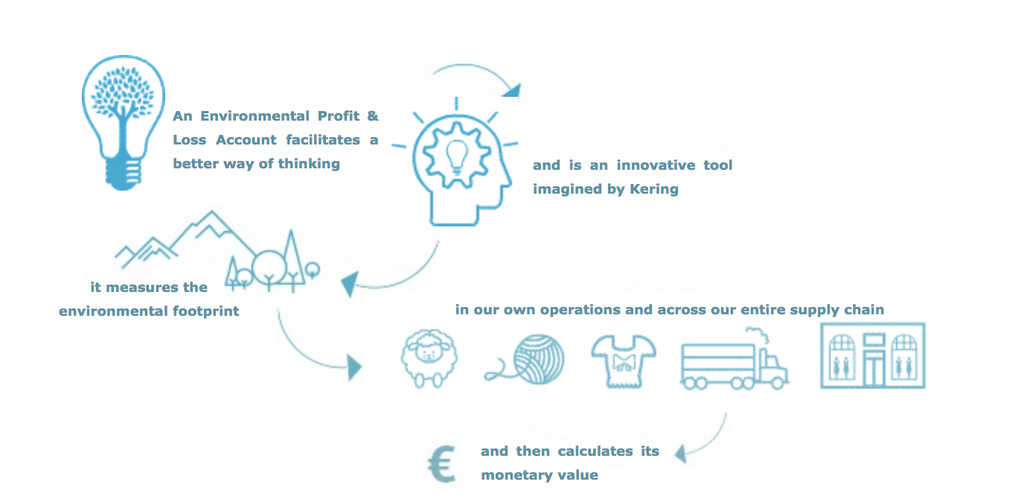

Environmental Profit & Losses (EP&L) was designed by Kering group (Puma) conceived by Puma chairman, Jochen Zeitz with the support of PricewaterhouseCoopers and Trucost. EP&L measures CO2 emissions, water consumption, air and water pollution, land use and waste generation throughout the supply chain (raw material extraction, processing, manufacturing, assembly, operations & retail), making the environmental impacts of the organisation’s activities visible, quantifiable and comparable. These impacts are then converted into monetary values to quantify the use of natural resources. The strong point of this methodology is that it is a first step in the process of ensuring that prices appropriately reflect the use of environmental goods and services. However, it is expensive to apply in practice.

Figure 5: What is an EP&L? (Kering, 2023)

The SeMA methodology (Sense Making & Accountability) according to ChatGPT, encourages individuals and teams to use their understanding and knowledge to make sense of the data, facts, and insights they are presented with in order to create meaningful decisions. It emphasizes accountability, both for individuals and for the organisation as a whole. This means that the individuals and teams involved in making decisions must be held accountable for the decisions they make and be able to explain why they chose the particular course of action. It also emphasizes transparency in decision making, which allows teams and individuals to understand the logic behind decisions and assess their effectiveness, and promotes collaboration and understanding between team members, allowing them to work together more effectively. However, the SeMA methodology model can be difficult to implement in large organizations due to its complexity and it can be difficult to ensure that all team members are held accountable for their decisions. It does not necessarily guarantee the best decisions, as it relies on the judgement of the individuals involved and it does not necessarily ensure that decisions are made in a timely manner.

The Universal Accounting methodology has stakeholder engagement at its core. It entails identifying stakeholders and listing their priorities, designing relevant indicators for each issue and developing the corresponding measurement process, which translates the data into monetary figures and aggregates them into income statements for each stakeholder. Indicators and strategies are divided into four accounting areas of governance: social rights, environment, society and financial. The overall profit and loss statements include all proposed indicators.The methodology considers all relevant stakeholders to an organization and their priorities in capital accounting. However, it can be difficult to apply in practice and provide findings that are comparable.

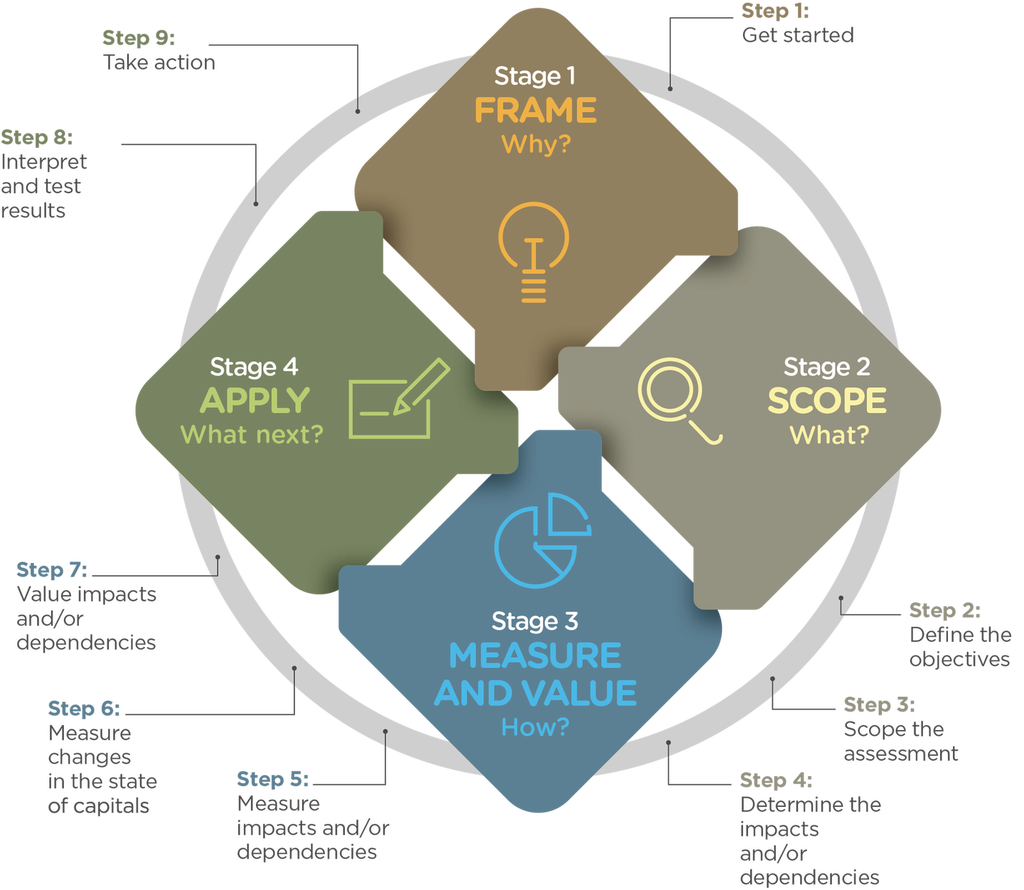

The Natural Capital Protocol was developed by the Capitals Coalition (formerly the Natural Capital Coalition), in partnership with the Cambridge Institute for Sustainability Leadership and another 37 organisations, following public consultation. The protocol provides a decision-making framework for businesses to identify, measure and evaluate their direct and indirect impacts and dependencies on natural capital, including those pertaining to risk management, supply chain management or product design. The framework explores four stages broken into nine steps, with questions to be answered when integrating the value of natural capital into the organizational process. It also has sector guides and supplements e.g. forest products, food & beverage, finance, apparel and biodiversity to support organisations in applying it. The protocol has many strong points. It is iterative and can be adapted and adjusted to each user; it is applicable to any business sector, to organisations of all sizes and in all operational geographies; it broadens the quantity and quality of business-relevant information available to decision-makers, to allow for educated decision-making; and it provides an internationally standardized framework for the identification, measurement and valuation of impacts and dependencies on natural capital, in order to inform organization decisions. However, the Protocol is an internally focused tool helping business prepare for future reporting and disclosure; it does not provide guidance on external reporting or disclosure.

Figure 6: The Natural Capital Protocol (Capitals Coalition, 2023)

The concept of the Triple Bottom Line was developed by John Elkington in the mid-1990s and was renamed to People, Planet, Prosperity (3Ps). It is an accounting framework that incorporates three dimensions of performance: social, environmental and financial. It measures an organisation’s profitability and shareholder values by considering its social, environmental and financial capital and can be used by any type of organisation, including businesses, not-for-profit and government entities. The framework is flexible to apply as there are no standard measures that comprise each of the three categories, so it can be adapted to the needs of different entities, projects, policies and geographies. It can also be case/project specific and can allow for a broad scope to measure impacts. Furthermore, it helps an organisation to measure, benchmark, set goals, improve and evolve into more sustainable systems and models. However, there is no universal standard method for calculating it – options include monetizing all its dimensions; using an index; using separate sustainability metrics for each dimension; etc. This makes it challenging to apply consistently in practice e.g. making an index that is comprehensive and meaningful; identifying suitable variables for the index; identifying suitable metrics; monetizing environmental and social assets accurately; finding applicable data. As a result the findings are not always comparable.

Figure 7: People, Planet, Prosperity (Synergy CMC, 2023)

Evolution of the concept of TCA

The importance of incorporating environmental and social dimensions into corporate decision-making and financial disclosures is gaining traction, in support of many existing frameworks and standards in the sustainability space. Case in point that the IFRS is developing its own two disclosure standards; one on General Requirements for Disclosure of Sustainability-related Financial Information (draft IFRS S1) and one on Climate-related Disclosures (draft IFRS S2), incorporating industry-based disclosure requirements from the Sustainability Accounting Standards Board (SASB) standards. These draft standards which tackle financial disclosures on environmental, social and governance issues, are expected to be launched in early 2023.

Furthermore, the newly formed Taskforce on Nature-Related Financial Disclosures (TNFD) is developing a framework that will enable companies and financial institutions to integrate nature and biodiversity into decision-making and reporting. According to the TNFD, nature and biodiversity are impacted by and impact organisations; their loss can be a major risk to organisations, while positive investments can be opportunities for organisations. This initiative is even more pertinent following the 15th Conference of Parties (COP) to the UN Convention on Biological Diversity, which adopted the “Kumming-Montreal Global Biodiversity Framework (GBF)” in December 2022. The GBF includes four goals and 23 targets for 2030 on nature and biodiversity, making it a landmark global agreement.

TCA is also a priority for the European Union, as well as globally for the World Bank, in collaboration with the UN, which are focusing on economic, green and socio-economic recovery, post COVID-19, and are pushing for natural capital accounting and social capital accounting to become the norm for corporate reporting, alongside the financial elements.

Utilising the universal business language of accounting to shift norms and promote corporate sustainability

Moving to triple capital accounting will require a paradigm shift with major transformations for the corporate world across borders. However challenging this may be, it will also create strong opportunities; access to new markets, products and services; managing of risks; added value to the brand and image of organisations; compliance with upcoming legislation; even attracting new clients and talent.

While the methodologies for TCA presented in this article vary, they do align in their ambition to incorporate environmental and social dimensions into financial reporting. Organisations definitely have a long way to go until this type of accounting becomes mainstream. Fact remains however that the organisations that wish to survive and even thrive in the corporate world, those who want to be active and not passive stakeholders, will need to move beyond a focus on just financial capital and rethink how they can account for and preserve all three capitals, redesigning their business model to be circular and sustainable.

Written by Laurent Le Pajolec, Member of the Board at EXCO A2A Polska Sp. z o. o and Christina Tsiarta, Head of Sustainability, ESG and Climate Change Advisory Services at Kreston Ioannou & Theodoulou

Main image: Laurent Le Pajolec, Member of the Board at EXCO A2A Polska Sp. z o. o