News

NEWS analysis

Pricing strategies struggle amid supply chain chaos

Over a fifth of accountancy employers are seeking remote talent

Once an industry established on strong office culture, the finance profession has adapted their previous working policies to reflect the ‘new norms’ in a post-pandemic world of work.

Recruitment experts, Hays’ March 2022 Quarterly Insights Survey, which received over 9,000 respondents – with over 1,000 respondents from those working in accountancy and finance – revealed that a significant 79% of employers now offer a hybrid form of working, of which 27% offer complete flexibility, leaving it up to employees to choose how frequently they come into the office.

Perhaps slightly more surprising is the fact that over a fifth (21%) of employers surveyed stated that they would look to hire fully remote talent within the next year. As a result of the new working practices, 57% of companies are rethinking the way the workplace is used – whether that’s downsizing, offering a more collaborative workspace, or implementing hot-desking.

Karen Young, Director of Hays Accountancy & Finance, comments: “What can be drawn from our latest Quarterly Insights Survey is that an overwhelming majority of finance professionals would opt for an organisation that offers hybrid working – 62% stated that hybrid working is their preferential policy, with 23% selecting fully remote working.

Perhaps even more telling is the fact a sizeable 82% of employees positively stated that since hybrid working has been applied, their work-life balance has improved.

As competition for finance professionals continues to heat up – employers need to continually address their offering to make sure they can attract top talent. Aspects such as flexibility are almost as important as salary – so employers need to make sure they are promoting their offering.”

IFRS Foundation Trustees appoint four members to ISSB

The IFRS Foundation has appointed a further four members to the International Sustainability Standards Board (ISSB).

The four members are Richard Barker, Verity Chegar, Bing Leng and Ndidi Nnoli-Edozien. All appointees will start their roles as full-time ISSB members in July 2022.

Richard Barker is currently deputy dean and professor of accounting at Saïd Business School, University of Oxford, UK. In this capacity, he leads Oxford Saïd’s sustainable business initiatives. He chairs the expert panel of Accounting for Sustainability (A4S) and has previously served as a member of several committees and bodies focused on corporate reporting in the UK and Europe, including the UK Corporate Reporting Council, the Financial Reporting Advisory Board and the European Accounting Association’s Accounting Standards Committee.

Verity Chegar has 20 years of experience in sustainable investment and stewardship, portfolio management and investment research with both asset owner and asset manager perspectives. She joins from the California State Teachers’ Retirement System (CalSTRS), where she leads the pension fund’s policy engagement on sustainable investment and stewardship issues and manages the fund’s work to reach its net zero ambition.

Bing Leng is currently a Director in the Accounting Regulatory Department of the Chinese Ministry of Finance, where he oversees sustainability reporting initiatives. He initiated and led the implementation of several reporting-related programmes, including the development of digital taxonomies to enable electronic reporting and plans focused on digitising the accounting profession.

Ndidi Nnoli-Edozien’s career has been focused on building connections between business and sustainable development, working across multinational and indigenous companies, public institutions and civil society organisations, in Africa and Europe, to initiate sustainable development initiatives. In her last role, she served as the inaugural Group Chief Sustainability and Governance Officer of Dangote Industries Limited—one of Africa’s largest manufacturing businesses. In this role, she was responsible for the developing the company’s sustainability culture, strategy and reporting across 14 countries.

The Trustees are committed to ensuring the ISSB has appropriate diversity and are at advanced stages of recruiting further board members. Appointments to bring the ISSB to quorum (eight members) will be announced shortly, with the aim of completing the inaugural appointments to the Board during the third quarter of 2022.

ICAEW president for 2022/23 appointed

The Institute of Chartered Accountants in England and Wales (ICAEW) has appointed Julia Penny as its president.

Penny will serve a one-year term until 2023, when she will then had over the role to Mark Rhys. Penny was first elected to the ICAEW Council in 2013 and has been an ICAEW board member since 2017.

Commenting on her appointment, Penny said: “When I set out to become a chartered accountant, I had little insight into the potential for the profession to be such a positive force for societal and environmental change. But chartered accountants can lead the transition to net zero, helping businesses to identify the changes necessary and providing assurance on green reporting.”

“We can also improve social mobility and champion greater inclusivity and diversity. Better decisions are made when we have more views around the table. Our professional qualification opens the door for individuals from all backgrounds to a seat around that table.”

Penny is ICAEW’s fourth female president and is passionate about achieving greater diversity of talent within chartered accountancy and making the profession more inclusive.

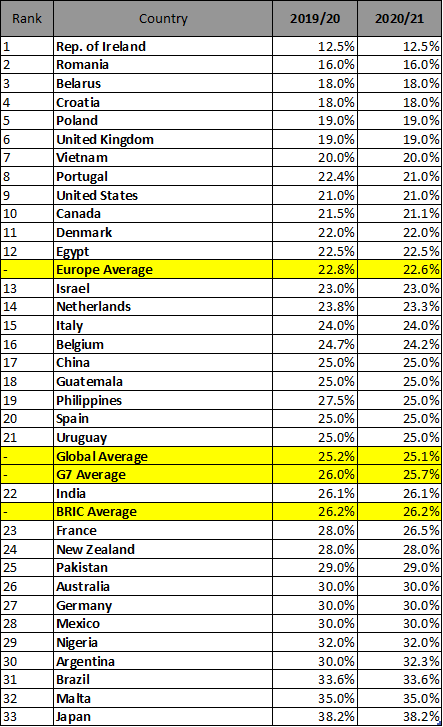

Global corporate tax rates hit new low of 25.1% with new trend of rising rates

Corporate tax rates in leading economies worldwide have fallen to an average of just 25.1%* shows a new study by UHY, the international accounting and consulting network.

However, with the Covid-19 pandemic leaving a gaping hole in the public finances of countries around the world, UHY says that the trend of declining corporate tax rates worldwide is likely to be over for the foreseeable future.

The UK government already announced its intention to raise corporation tax rates to 25% from April 2023, more than two percentage points higher than the European average. Argentina already increased its headline corporate tax rate from 30% to 35% in 2021. US President Joe Biden has also pledged to raise federal corporate income tax to 28%, after it was cut to just 21% by his predecessor Donald Trump in 2017.

Global corporate tax rates have been steadily decreasing over recent years, with the G7 average for a business recording profits of 1 million USD falling from 32% in 2014/15 to just 26% in 2020/21. Many countries sought to incentivise businesses to invest in their economies with attractive tax rates. France, often seen as a higher tax European economy, has lowered its headline rate from 31% to 26.5% in just the past three years.

Subarna Banerjee, Chairman of UHY, comments: “Countries around the world have wanted to remain competitive by keeping the tax burden on companies as low as possible in recent years. The cash strapped governments of 2022 will likely now be considering increasing taxes on corporates.”

“Public finances will have to be shored up somehow and corporates can be an easier target politically than individuals. Businesses worldwide should be prepared for their tax costs to begin to rise in the coming years.”

Could more corporate tax hikes be possible?

Developing nations surveyed by UHY typically already had higher corporate tax rates than their more economically developed counterparts. India’s tax rates hit 34% for the largest corporations, with Nigeria implementing a headline rate of 32%, and Argentina charging its resident companies 35% on their profits.

Experts question whether there is scope for some countries to raise taxes further. Japan already charges its companies up to 38.2%, and Malta has similarly high rates at 35%.

Lomme van Dam of Govers Accountants in the Netherlands says: “Governments should carefully balance their tax deficits with their economic recovery. Businesses paying punitively-high tax rates could lead to slower growth in employment, revenues and ultimately tax receipts.”

US’ economic outlook at 11-year low

The outlook for the US’ economy has tumbled to an 11 year low, according to the second-quarter AICPA Economic Outlook Survey.

The survey, which polls chief executive officers, chief financial officers, controllers, and other certified public accountants in the US, found inflation worries, a tight labour market and global fallout from the Russian invasion of Ukraine have all contributed to the economic outlook falling to its lowest level since 2011.

Only 18% of business executives expressed optimism about the U.S. economy’s outlook over the next 12 months, down from 36% last quarter. That’s less than during the initial shock of the Covid-19 pandemic two years ago (20% optimism) and the lowest it’s been since the third quarter of 2011, when it stood at nine percent.

A vast majority (97%) of respondents said there was at least some risk of recession within the next 12 months, with one-in-four calling it a significant possibility.

Inflation was the top concern of business executives for the third straight quarter, with labour costs seen as the main driver. Salary and benefit costs are now expected to increase at a rate of 4.4%, higher than at any time since before the Great Recession. Energy costs and interest rate hikes are also rising contributors to inflationary pressures, executives say.

Association of International Certified Professional Accountants executive vice president of business engagement and growth Tom Hood said: “We’re still seeing residual stresses on supply chains from the pandemic and that’s now been coupled with the impact of sanctions and business wind-downs involving Russia. Those global dislocations, a volatile pricing and cost environment, and the continuing impact of workplace shifts such as the Great Resignation are putting a lot of pressure on businesses and their finance teams.”

1 year anniversary of 6AMLD

Colum Lyons, CEO of ID-Pal, comments on the one-year anniversary of 6AMLD, “On 3 June 2021, it became mandatory for financial institutions to implement the European Union’s 6th Anti-Money Laundering Directive – 6AMLD – into their businesses. One year on, it’s clear robust AML procedures are more important than ever, with two thirds of UK businesses reporting to have fallen victim to fraud in the last two years.

“All financially regulated businesses, many of which process sensitive customer information daily, must ensure they are familiar with 6AMLD best practices and adjust their AML compliance processes accordingly. Fraudsters will exploit every possible loophole to achieve their goals. To combat this, businesses should use multi-layered global solutions such as ID-Pal that can stop fraud at the source. By seamlessly performing multiple checks in real-time on identity documents and the documents holder, organisations can protect themselves and their customers, reducing both upfront and reputational costs to their business.”

High pressure driving exodus from financial services

Almost a third (31%) of financial services and banking professionals are planning to leave the industry due to high pressure, according to a report from LemonEdge, a global digital accountancy platform for the private capital and venture capital industry.

While some workers have experienced positive benefits of hybrid working, a third (33%) of financial services and banking professionals state levels of burnout have increased due to changes in work environment since the pandemic and the working from home hybrid model began. Within this, one in six (14%) said burnout has increased exponentially.

When researching why workers are planning to leave their positions in record numbers, the study found that financial services and banking professionals state a heavy workload (42%) is the main contributor to feeling heightened pressure within their role. This is closely followed by manual processes (36%), long working hours (32%), tight deadlines (26%), and increasing demands from management (25%).

In order to overcome the problem, a third (33%) of financial services professionals are in agreement that a reduced workload would reduce burnout. Other solutions include time off work (27%), more support from management (25%), and faster, more efficient technology (23%).

Co-founder and CEO of LemonEdge Gareth Hewitt said: “An exodus of industry professionals is a sure sign that levels of burnout have reached an unacceptable scale. Any experience of burnout is serious and with thousands of employees planning to leave the industry as a direct result of high pressure, it should be a clear warning to firms before they risk losing valuable talent.

“The risk of burnout to employers is huge, and there are simple measures firms can introduce to reduce the risk of burnout, making the lives of their employees much simpler, easier, and with less stress. Firms need to be aware of the impact absenteeism and presenteeism will have on both their employees and business productivity.

“Just because you’re working from home, or in a hybrid model, doesn’t mean you can’t enjoy time off. With one in four (23%) asking for faster or improved technology to eliminate manual processes, firms need to look at their approaches to improve the lives of their staff. In this day and age, technology, not only can but should, provide the automation and flexibility that can contribute to reduced stress, reduced working hours, and lower risk of burnout. At LemonEdge we are passionate about providing the tools and technology that enable financial services professionals to get home on time.”